How to Estimate Your EFC and Plan for College Costs

Estimating your Expected Family Contribution (EFC) is crucial for college planning, as it determines your eligibility for financial aid and helps you understand the costs you may need to cover.

Planning for college involves understanding various financial aspects, with the Expected Family Contribution (EFC) being a key component. Let’s explore how to estimate your Expected Family Contribution (EFC) and plan for college costs effectively.

Understanding the Expected Family Contribution (EFC)

The Expected Family Contribution (EFC) is an estimate of how much your family can contribute to college costs. It’s based on your family’s income, assets, and other factors. Understanding this figure helps in financial planning for higher education.

What is EFC and why does it matter?

EFC, now formally known as the Student Aid Index (SAI), helps colleges determine your financial aid eligibility. It influences the amount of grants, loans, and work-study opportunities you may receive. The lower your EFC, the more financial aid you’re likely to qualify for.

Factors that influence your EFC

Several factors affect your EFC, including:

- Income: Both the student’s and parents’ income are considered.

- Assets: Savings, investments, and other assets are taken into account.

- Family Size: The number of family members in the household.

- Number in College: The number of family members attending college at the same time.

Knowing these factors can help you estimate your EFC and plan your finances accordingly. Understanding the financial landscape related to education is essential.

Gathering Necessary Financial Information

Before you calculate your EFC, it’s important to gather all necessary financial documents. Having this information readily available will make the estimation process smoother and more accurate.

Required documents for EFC estimation

To estimate your EFC, you’ll need the following documents:

- Tax Returns: Both student and parent tax returns (e.g., Form 1040).

- W-2 Forms: Records of annual earnings.

- Bank Statements: Checking and savings account balances.

- Investment Statements: Information on stocks, bonds, and other investments.

Finding income and asset information

Locate your Adjusted Gross Income (AGI) on your tax return. This is a key figure used in EFC calculations. Gather statements from banks and investment firms detailing your assets. These records provide a clear picture of your financial standing.

With these documents in hand, you’re ready to start estimating your contribution towards college expenses, paving the way for informed financial strategies.

Using the FAFSA Forecaster Tool

One of the easiest ways to estimate your EFC is by using the FAFSA Forecaster Tool, now known as the StudentAid Estimator This tool provides an estimate based on the financial information you input.

How to access the FAFSA Forecaster online

The StudentAid Estimator is available on the Federal Student Aid website. Simply search for “StudentAid Estimator” on the official government website to find the tool.

Step-by-step guide to inputting data

When using the StudentAid Estimator, follow these steps:

- Enter family income: Provide accurate income details for both parents and students.

- Report assets: Include savings, investments, and other assets.

- Provide family information: Number of family members and students in college.

- Review results: The tool will provide an estimated EFC based on your input.

This step-by-step approach makes the estimation process manageable and transparent, enabling you to proactively approach financial discussions.

Understanding EFC Calculation Formulas

While the FAFSA Forecaster provides a quick estimate, understanding the underlying calculation formulas offers deeper insights. This knowledge can help you anticipate how various financial decisions might impact your EFC.

Simplified Needs Test (SNT)

The Simplified Needs Test (SNT) is used for families with lower incomes. If a family meets the SNT criteria, certain assets aren’t considered in the EFC calculation, potentially lowering the estimated contribution.

Regular EFC Calculation

The regular EFC calculation considers both income and assets. A percentage of income and assets are assessed to determine the family’s ability to contribute. Understanding how these percentages are applied can aid in financial planning.

Understanding these formulas provides you with a more detailed perspective, allowing for proactive adjustments to potentially optimize your EFC and overall financial strategy.

Strategies to Reduce Your EFC

While you can’t drastically change your financial situation overnight, certain strategies can help reduce your EFC. These strategies involve carefully managing assets and income to maximize financial aid eligibility.

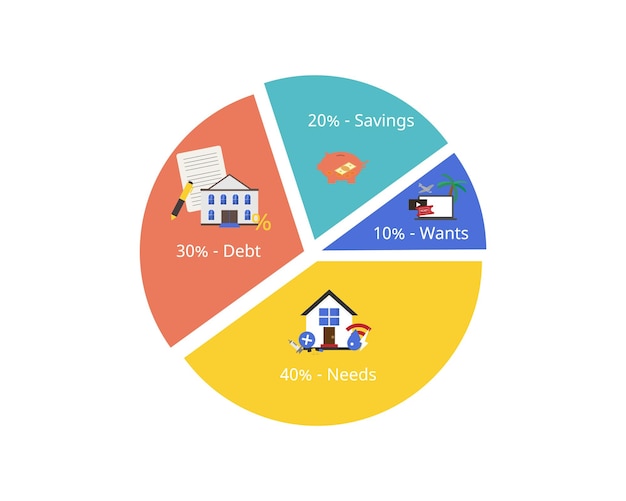

Maximizing retirement contributions

Contributions to retirement accounts, such as 401(k)s and IRAs, are not counted as assets in the EFC calculation. Increasing these contributions can lower your reported assets, potentially reducing your EFC.

Paying down debt

Debt isn’t considered an asset, so paying down debt can free up income and reduce assets. Focusing on reducing debt proactively can have a positive impact on your overall financial profile.

- Prioritize retirement savings: Contribute to tax-advantaged retirement accounts.

- Reduce taxable income: Explore tax deductions and credits.

- Consult a financial advisor: Seek professional advice for personalized strategies.

These practical steps can help position you favorably when estimating your EFC, enhancing your college financial planning.

Planning for College Costs Beyond EFC

While understanding and estimating your EFC is crucial, it’s equally important to plan for college costs beyond the EFC. This involves exploring other sources of funding and understanding the true cost of attendance.

Exploring scholarships and grants

Scholarships and grants are excellent ways to reduce your out-of-pocket expenses. Research opportunities from federal, state, and private sources. Many organizations offer scholarships based on merit, need, or specific interests.

Understanding the true cost of attendance

The true cost of attendance includes tuition, fees, room and board, books, and other expenses. Understanding this cost helps you create a realistic budget and plan your finances effectively. Consider the total financial commitment when choosing a college.

By diversifying financial strategies and thoroughly assessing the full costs, you create a more comprehensive and robust college financial plan.

[Início da área da tabela minimalista]

| Key Point | Brief Description |

|---|---|

| 💰 Understanding EFC | EFC determines financial aid eligibility; lower EFC means more aid. |

| 📝 Gathering Documents | Collect tax returns, W-2s, and bank statements for accurate EFC estimation. |

| 💻 Using FAFSA Forecaster | Utilize the StudentAid Estimator for a quick EFC estimate. |

| 💡 Reducing EFC | Maximize retirement contributions and pay down debt to potentially lower EFC. |

How to Estimate Your Expected Family Contribution (EFC) and Plan for College Costs

▼

The SAI, previously known as the Expected Family Contribution (EFC), is an estimate of how much a student and their family can contribute to college costs, used to determine financial aid eligibility.

▼

The StudentAid Estimator is available on the official website of the Federal Student Aid. Search for “StudentAid Estimator” on the government website to locate the tool.

▼

You’ll need tax returns, W-2 forms, bank statements, and investment statements to accurately estimate your Expected Family Contribution (EFC). Having these documents ready will streamline the process.

▼

Contributions to retirement accounts like 401(k)s and IRAs are not considered as assets in the EFC calculation, which can potentially lower your estimated family contribution.

▼

Maximize retirement contributions, pay down debt, and seek professional financial advice to optimize your financial profile and potentially lower your Student Aid Index (SAI).

Conclusion

Estimating your Expected Family Contribution (EFC) and planning for college costs is a multi-faceted process that requires careful consideration and proactive strategies. By understanding the factors that influence your EFC, gathering necessary financial documents, and exploring various funding options, you can create a comprehensive financial plan that makes college more attainable.